The EOS network continues to be the most high profile opposition to Ethereum’s supremacy as the go-to wise agreement and Dapp hosting blockchain platform. The EOS token is presently the Fifth biggest crypto possession, with a market cap of over $4.2 billion (compared with Ethereum’s $21 billion).

It presently trades at $5.40, down|74% from a perpetuity high of $2070(Index), accomplished on April 29 th 2018, simply over 4 months earlier. Daily exchange-tracked trading volumes are likewise down roughly 85% from this peak.

It has actually been a sharp drop in belief and cost efficiency over a reasonably brief time duration. The favorable belief around the network’s mainnet roll out on June the 9th, was terribly dented by an apparently botched launch and immediate governance challenges following its detachment from the Ethereum blockchain.

The guarantee of the EOS mainnet had actually sustained upward cost momentum in the very first half of the year, as the brand-new EOS blockchain was allegedly going to provide an innovative Dapp experience for users and designers– with faster deal times, steady governance and enhanced security. The pre and post launch concerns that afflicted EOS changed this optimism with FUD, nevertheless.

That aside, Dapp and user activity are getting with EOS throughput quicker than lots of PoW networks consisting of Ethereum– considering that August 14 th, EOS cost is up|24%, while over the very same duration ETH’s cost has actually fallen|17%.

Exchanges and trading sets

The most popular trading sets for EOS are crypto-to-crypto with the USDT/EOS and BTC/EOS sets comprising over 75% of day-to-day trading volumes, with integrated 24 hr volume of the 2 sets worth over 500 million USD. The next 5 most popular trading on-ramps for EOS are a mix of crypto and fiat alternatives with Ethereum, United States dollar and Korean Won trading alternatives all handling substantial day-to-day volumes.

The most popular exchanges for trading USDT/EOS are Okex, Binance and Huobi— internationally popular platforms understood for their liquidity, promos and variety of trading alternatives. Integrated, these exchanges manage over $225 million worth of day-to-day trading volume of EOS sets.

Innovating the agreement design

The EOS Delegated Proof of Stake model was very first developed by blockchain evangelist Dan Larimer in2015 At the time the concept of eliminating miners and processing power competitors from a blockchain in favour of constant conversation in between block manufacturers, in addition to the issuance of ballot rights to the token holding neighborhood, was plainly foreign.

Nevertheless, the proposed enhancements to a few of the intrinsic defects developed within standard PoW and PoS designs rapidly acquired traction with lots of crypto observers.

Delegated Evidence of Stake is a kind of technological democracy, or on-chain governance, where staked token holders assign their tokens for voting-in block producing delegates (more tokens staked, more ballot rights). Block manufacturers then settle deals as miners would on other blockchains, with the remainder of the network having an agreement vote on the block’s credibility.

In EOS, block manufacturers utilize SHA-256 to create the absorb then sign it utilizing either the P1 or K1 secret. Every non-zero wallet in EOS has ballot rights, and elections are run continually, with a waiting swimming pool of delegates, all set to action in and take control of as one of EOS’s unique group of block manufacturers, need to efficiency on the network ever drop.

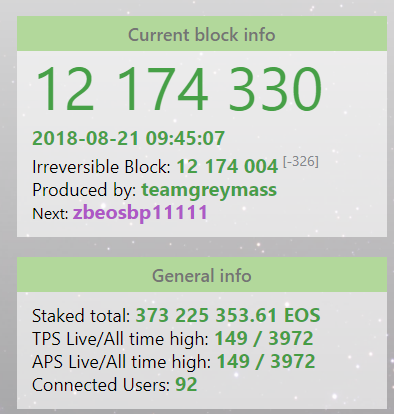

Presently,|53% of the overall EOS in flow has been staked for voting, showing that near to half of the EOS token holding neighborhood is either indifferent in the governance of the network, or is merely delighted to maintain the present status quo of miners.

No matter the factor, this significantly decreases the stakes for the EOS delegates/block manufacturers to keep high efficiency levels. Considered that neighborhood tracking is developed to be the main look at node efficiency, the low-ish citizen turnout is worrying.

No matter the factor, this significantly decreases the stakes for the EOS delegates/block manufacturers to keep high efficiency levels. Considered that neighborhood tracking is developed to be the main look at node efficiency, the low-ish citizen turnout is worrying.

Delegates/nodes likewise keep regular interaction about essential network choices with each other and the neighborhood, through group video calls, regular AMAs (ask-me-anything) and social networks conversations. This design of governance has actually been described as ‘consensus by conference call‘ and critics have actually questioned its effectiveness.

However, this system does provide substantial benefits. With just 21 nodes in the network, compared with 9000 on Bitcoin’s network, agreement on deals is accomplished quicker and with much less power taken in.

There are presently 4,383 active addresses in the EOS network– a figure overshadowed by the 320,341 on Ethereum and 613,352 on the Bitcoin. Nevertheless, those addresses seem fairly active. In a current 24 hour duration, for instance, 128,057 payments were made on the EOS network, compared with 287,623 on Ethereum and 341,989 on Bitcoin– showing that although EOS appears to have far less users than its bigger rivals, based upon deals and payments they are more proportionally more active.

Remarkably, the most active Dapp in the whole blockchain environment is EOS hosted ‘EOSbet‘ which in a current 7 day duration tape-recorded volume of 7,157,86929 EOS tokens, throughout 1,215,926 deals, with a worth of|$465 million. This overshadows the varieties of Ethereum’s most popular Dapp IDEX, which had a deal volume of 36,602 in the very same duration– worth|$104 million.

While observers might question the stability of an environment that depends on a dice rolling game of chance for the huge bulk of its deals, the volume is nevertheless genuine, with EOSbet having little, however responsive, twitter and reddit neighborhoods.

In addition, even if betting Dapps are not a reflection of how the EOS environment is developed to be utilized, the level of activity on EOSbet functions as a helpful tension test on the capability of the blockchain to manage heavy day-to-day deal volume. Moreover, Blockchain based gambling ICOs reportedly raised 776 million dollars in June 2018 which bodes well for a network that has actually shown its capability for dealing with high volumes.

The EOS network monitor shows that deal volumes have actually been as high as 3972 per second in the past. Based on numbers starting from April 2016, the Bitcoin blockchain’s deals per second has actually never ever been greater than 20, with the average over this time duration a really modest|2.5.

Network basics and efficiency aside, the most significant criticisms of EOS are more ideological. Considered that deals are settled by such a little group of nodes, that are not confidential, and have actually been designated the rights to do so, EOS loses outright censorship resistance.

EOS likewise proposes that the 21 nodes, can reverse deals that do not line up with the EOS approach, or appear harmful, offered the tight knit nature of the node swimming pool. This basically suggests deals on EOS are not long-term or immutable This breaks the decentralized, anti-establishment suitables of initial PoW approaches and continues to make the EOS design a difficult sell to blockchain idealists.

Intriguingly, there is an argument that EOS is, in reality, more decentralized than a lot of its PoW equivalents. Deals on EOS are confirmed uniformly throughout 21 miners, indicating the processing power and block benefits stay & steady continuous, without a single entity in the group efficient in cornering the hashrate in the network.

With big PoW networks it appears unavoidable that as hashrate boosts, and mining on the network ends up being gradually more processor extensive, big resource-rich mining swimming pools will start to control hash rate and block production.

This is precisely how things have actually turned out with Bitcoin, as a group 7 mining swimming pools control– comprising|82% of the network’s hashrate.

This plainly seems a more central circulation of power as compared EOS, nevertheless, the design keeps the aspect of competitors. Anybody can end up being a miner on Bitcoin and challenge the swimming pools, it is not a permissioned network like EOS.

This plainly seems a more central circulation of power as compared EOS, nevertheless, the design keeps the aspect of competitors. Anybody can end up being a miner on Bitcoin and challenge the swimming pools, it is not a permissioned network like EOS.

In addition, miners on Bitcoin have far less power over deals than delegates on the EOS network, since of the competitors. The network is developed to be trustless, and there is no requirement for the block manufacturer’s visions to line up with the Bitcoin neighborhood. In this sense, Bitcoin’s PoW design keeps a component of pureness and unbiasedness versus DPoS.

Technical analysis

Mean Reversion and Long Term Pattern s

First, on the 1D chart, cost is presently experiencing a short-term bounce and holding at|$5.40 Nevertheless, considering that late-April 2018, regardless of the remarkable buzz, EOS has actually been restricted within a sharp sag (regression channel) with a Pearson R Connection in between time and cost of 0.92 In addition, the volume flow indicator(VFI) has actually stayed underneath 0 considering that preliminary estimation back in July.

Moreover, the unfavorable VFI pattern reveals no indications of easing off in the future (black arrow). The VFI analysis is a worth above 0 is bullish and listed below 0 is bearish, with divergences in between cost and oscillator being high possibility signals.

2nd, regrettably for EOS, possession costs constantlymean revert Hence, if the present pattern continues, cost is most likely to recuperate and forth within the regression band, however is predestined to fall back to the|$1 level (black rushed line).

Third, to this day, when cost volatility has actually compressed (bollinger bands) and cost “based out” (horizontal black line), a down breakout has actually generally taken place (orange arrows). Visual heuristics like the abovementioned can be unsafe in trading offered they are “general rules” instead of guidelines confirmed in information over an appropriate period. Nevertheless, in EOS’s case, this heuristic lines up with our direct pattern analysis, which provides a minor increase in possibility of reoccurrence. Regrettably, for EOS, this falls in line with the previous mean reversion supposition and anticipated cost target of|$1.

Third, to this day, when cost volatility has actually compressed (bollinger bands) and cost “based out” (horizontal black line), a down breakout has actually generally taken place (orange arrows). Visual heuristics like the abovementioned can be unsafe in trading offered they are “general rules” instead of guidelines confirmed in information over an appropriate period. Nevertheless, in EOS’s case, this heuristic lines up with our direct pattern analysis, which provides a minor increase in possibility of reoccurrence. Regrettably, for EOS, this falls in line with the previous mean reversion supposition and anticipated cost target of|$1.

Last, there are 2 rays of positivity for cost. One, considering that mid-August, cost has actually started to form a minor uptrend (bottom orange pattern line), which was protected throughout this last downtick from the Goldman Sachs news. Second, a flag pattern is forming from the abovementioned uptrend which has the capability to breakout to the advantage (green arrow) or disadvantage (red arrow). The advantage possibility would be increased by an increase in VFI to 0 over the coming days and weeks.

Last, there are 2 rays of positivity for cost. One, considering that mid-August, cost has actually started to form a minor uptrend (bottom orange pattern line), which was protected throughout this last downtick from the Goldman Sachs news. Second, a flag pattern is forming from the abovementioned uptrend which has the capability to breakout to the advantage (green arrow) or disadvantage (red arrow). The advantage possibility would be increased by an increase in VFI to 0 over the coming days and weeks.

Ichimoku Clouds with Relative Strength Indication (RSI)

The Ichimoku Cloud utilizes 4 metrics to figure out if a pattern exists; the present cost in relation to the Cloud, the color of the Cloud (red for bearish, green for bullish), the Tenkan (T) and Kijun (K) cross, Lagging Period (Chikou), and Senkou Period (A & B). The status of the present Cloud metrics on the 1D frame with singled settings (10/30/60/30) for quicker signals is bearish; cost is listed below the Cloud, Cloud is bearish, the TK cross is bearish, and the Lagging Period is listed below the Cloud and touching cost.

A standard long entry would accompany a cost break above the Cloud, called a Kumo breakout, with cost holding above the Cloud. From there, the trader would utilize either the Tenkan, Kijun, or Senkou A as their tracking stop.

At the time of composing, EOS is sitting at|$5.45 after striking off Kijun resistance at $5.54 In late-August, cost was making a constant healing and possibly marching to a Kumo breakout effort when it fell quickly from the news that Goldman Sachs was not opening its own crypto trading desk This news sent out cost into a tailspin from near $6.67 to its present levels. One favorable note is that with this current fall, RSI is back near oversold area and presently trending greater. This might recommend that a short-term cost revival is upon EOS, with an ultimate Kumo breakout retest. Nevertheless, the possibility for an effective Kumo breakout stays low to medium.

For either situation, the vital assistance level is $4.25(2nd “base” line). If that assistance stops working, the next, significant assistance levels are $3, $2, and $1. In the not likely occasion of a Kumo breakout, cost will have to breach $6.77 with targets of $7.83 and $9.

The status of the present Cloud metrics on the day-to-day timespan with doubled settings (20/60/120/30) for more precise signals is bearish; cost is listed below the Cloud, Cloud is bearish, the TK cross is bearish, and the Lagging Period is listed below the Cloud and touching cost.

The status of the present Cloud metrics on the day-to-day timespan with doubled settings (20/60/120/30) for more precise signals is bearish; cost is listed below the Cloud, Cloud is bearish, the TK cross is bearish, and the Lagging Period is listed below the Cloud and touching cost.

Once Again, in the not likely occasion of a Kumo breakout in the near-term, cost will have to breach $10 with targets of $1150 and $1230

Conclusion

The EOS token has actually lost a few of its shine following a difficult primary network launch previously in the year. Nevertheless, with its network presently totally working, it has actually kept outstanding throughput and presently hosts the most popular Dapp in the whole blockchain environment.

The network, nevertheless, will likely continue to deal with ideological distinctions with cross-sections of the crypto neighborhood since of its trust based agreement algorithm. Secret obstacles EOS need to resolve moving forward are the inadequacy of its network governance and the low citizen turnout among EOS token holders.

The technicals for EOS are securely bearish regardless of the buzz, favorable cost pattern considering that mid-August, and helpful RSI. Nevertheless, both, the sensible short-term trader (10/30/60/30) and longer term trader (20/60/120/30), on the 1D chart, will wait for a favorable TK cross and Kumo breakout above $6.77 and $10, respectively, prior to going into a long position. The vital assistance level is $4.25 with the next substantial ones at $3, $2, and $1.

Disclaimer: This analysis has actually been developed for informative and instructional functions just. Readers are recommended to perform their own independent research study into specific possessions prior to buying choice.

About the authors

Christopher Brookins

Christopher Brookins

Christopher Brookins is the creator and CEO of Pugilist Ventures, a quantitative financial investment company concentrated on digital possessions and blockchain innovation. Chris has a deep understanding and special point of view on digital possessions formed by his polymath experience in equity trading, credit investing, and company advancement at 2 West Coast start-ups (one gotten). He has actually been associated with the blockchain neighborhood considering that2014 Follow @chris__brookins

Aditya Das

Aditya Das is Brave New Coin’s internal market expert. Raised in Dubai, UAE, he holds a post-graduate honors degree in Economics from the University of Auckland and a Bachelor’s Degree in Economics from the University of Sussex. Prior to signing up with BNC his newest functions were as a scientist and Economics tutor at the University of Auckland. Follow @Quartlifecrypto