By Bitget CEO Sandra

Derivatives items have actually been playing a substantial function in the international financing market. As the principle of decentralization experienced fast advancement and slowly acquired larger acknowledgment amongst users in the last few years, decentralized derivatives trading has actually naturally turned into one of the most appealing markets. So is it possible for decentralized derivatives exchanges to interrupt their central equivalents in the brief to medium term? Here are a few of my ideas and I want to share them with you.

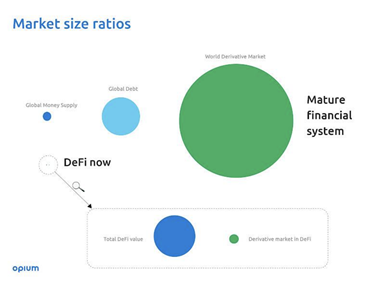

In the conventional monetary sector, derivatives are categorized into the following classifications by various item types: forwards, futures, alternatives and swaps. Their underlying possessions can be stocks, rate of interest, currencies and products. The notional worth of the total derivatives market in 2020 is approximately $840 trillion, compared to $56 trillion for the equity market and $119 trillion for the bond market. And the size of the derivatives market is 4 to 5 times bigger than that of its underlying possessions.

While in the crypto world, the majority of the derivatives deals take place in central exchanges in the types of quarterly futures, continuous futures (likewise called continuous swaps) and alternatives.

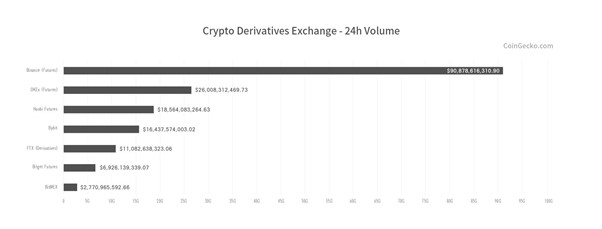

According to Coingecko, Binance, OKEx, Huobi, Bybit, FTX, Bitget and BitMEX are the world’s top7 derivatives exchanges. Take Binance as an example, its area trading volume in the last 24 h reached $23 billion while the derivatives trading volume struck $775, or 3.37 times the previous.

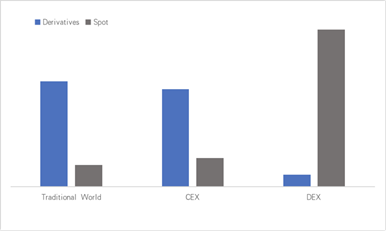

Things are rather various in decentralized exchanges (DEX). With an integrated 24- hour trading volume of $1.25 billion for Uniswap V2 and V3 and $96 million for the decentralized derivatives exchange represented by Continuous Procedure, futures trading volume represent just one-fourteenth of area trading.

The world’s top7 derivatives exchanges. Source: Coingecko

The volume of derivatives trading vs. area trading throughout various markets. Source: Insight Ventures

Presuming that decentralized derivatives can likewise reach 4 times the volume of area trading as in central exchanges, the space for development is huge. Nevertheless, from what we see now, business advancement of decentralized derivatives exchanges is far from pleasing.

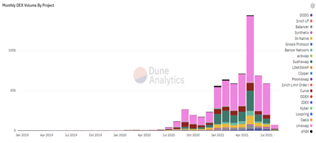

Trading information of decentralized derivatives exchanges. Source: Dune

Benefits and Drawbacks of Decentralized Derivatives Exchanges

In the decentralized world, there are generally 2 kinds of derivatives: futures and alternatives. Though index items, structured items and insurance coverages are likewise derivatives, they are not the focus for our function here. Compared to central organizations in the crypto area, decentralized derivatives exchanges have the following benefits:

- Property custody: The possessions of decentralized derivatives jobs are hosted on the chain. It is transparent and traceable, preventing abnormalities and default dangers of central organizations.

- Fairness: Set by wise agreements ahead of time, the trading guidelines can not be damaged in the back workplace, offering higher fairness for both celebrations to the deal.

- Self-governance: In decentralized derivatives exchanges, things like the charges to be charged, coins to be noted and advancement strategies can all be identified through neighborhood governance. Individuals associated with the decision-making procedure might delight in the advantages of job development.

Nevertheless, there are likewise immediate issues to be resolved.

- Efficiency: Derivatives trading needs real-time deals, which are challenging to accomplish through the existing on-chain options.

- Cost discovery: Derivatives trading is incredibly price-sensitive. Nevertheless, the mark costs and deal costs depend on the forecast of oracles.

- Threat control: Liquidation is a significant problem for both decentralized and centralized exchanges. Decentralized platforms likewise require to attend to the on-chain blockage triggered by severe rate volatility to make sure the liquidation procedure is sensible and effective, which is vital for the continued presence of derivatives platforms.

- Expense and liquidity: Margin trading with high leverages needs high liquidity of underlying possessions. The platform requires to prevent the effect expense of deals and develop an affordable cost schedule.

- Capital usage: a core requirement for traders to take part in derivatives trading is the capability to trade on margin with extra take advantage of, however the overcollateralization system presented by some artificial possession jobs as soon as again restricts the effective usage of capital.

- Privacy: On-chain information are traceable, yet institutional financiers wish to keep their positions and futures agreement address confidential.

Various Kinds Of Decentralized Derivatives Exchanges

In today’s market, decentralized futures derivatives have the biggest variety of job types and the most varied options, generally represented by continuous futures, which presently fall under 3 significant categories: AMM, order book and artificial possessions

AMM represented by Continuous Procedure

The AMM (Automated Market Making) based exchanges are generally transformed from the AMM design of Uniswap, such as vAMM and sAMM. It permits traders to connect with the possessions in a physical or virtual possession swimming pool to long or brief.

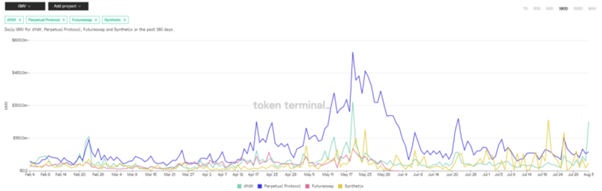

GMV Information of mainstream decentralized derivatives platform. Source: Token terminal

This type is generally represented by Continuous Procedure. According to Messari, Continuous Procedure uses up 76% of the continuous futures market and its income size in July was the seventh-largest of all Defi jobs, behind Sushiswap. Nevertheless, the trading volume and income do not properly show its real market share as it is challenging to compute just how much is contributed by the wash trading arised from the trans-fee mining started in February this year.

Based upon a virtual liquidity swimming pool called vAMM. The Continuous Procedure utilizes the formula of X * Y= K to imitate rates. Traders can input USDC as security to the Vault. So external liquidity service providers are not needed. It is likewise a method to mint artificial possessions. With the only USDC in the swimming pool, there is no real exchange in between 2 real currencies. The quantity of funds streaming in and out of the Vault, along with the returns, are computed utilizing a mathematical formula based upon the rate of the trading set at the time of their entry and exit.

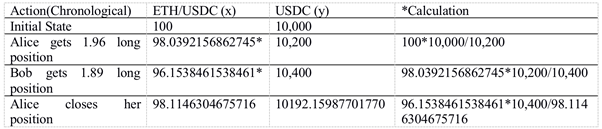

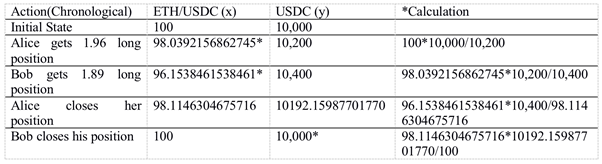

Let’s walk through an example trade discussed by the job white paper.

- X * Y= K , The rate ratio of ETH and USDC is Y/X =-LRB- *********************************************************************************************************************)

Presuming there are 10000 USDC in the Vault. X =-LRB- *********************************************************************************************************************) , K =-LRB- *********************************************************************************************************************) *10000 Alice utilizes 100 USDC as the margin to open a 2x leveraged long position on ETH;-LRB- ******).

- After that, the quantity of USDC in the vAMMs will end up being 10,200(10,000+100 * 2), the quantity of ETH/USDC will end up being 98.04(100 *10,000/10,200), and the position Alices opens is 1.96 ETH (100-9804).

- Following Alice, Bob likewise utilizes 100 USDC to open a long position with 2x take advantage of. His position size will be 1.89 ETH (9803-9615) utilizing the exact same estimation. Keep in mind that the rate of ETH boosts due to Alice’s opening, for that reason the typical holding expense of Bob is greater than that of Alice.

- After Bob gets his long position, the rate of ETH more climbs up. Alice closes her position and understands a revenue of 7.84 USDC (10400– 96.15 *10,400/(9615 +1.96)- 200)

- Seeing Alice earns a profit, Bob wishes to close his position too, just to discover that he lost -7.84 USDC (1019215-9811 * 10192.15/ (9811+ 1.88)-200) after closing his position.

From the above example, we can see that a person trader’s gain equates to another trader’s loss. All traders in the swimming pool are counterparties with their earnings computed based upon the virtual AMM design. This design has the following functions:

- AMM design does not need making use of an external Oracle for rate discovery. Rather, the rate will reach stability through the well balanced activities of arbitrageurs in between CEX and DEX. Though the method can prevent the danger of Oracles, there might be a severe variance in between possession costs in the exchange and outdoors market in the lack of arbitrageurs, resulting in the liquidation of margin traders.

- In the Continuous job, the K-value is a floating worth set by the group. If the K-value is too little, the depth of the swimming pool will be decreased. However if the worth is too big, the rate change in the exchange will be too small to match the outdoors rate. For that reason, the setting of the K worth will considerably affect the operation of the AMM design.

- In the AMM design, big orders will sustain higher effect expenses to the swimming pool, particularly for price-sensitive futures traders, whose income will be considerably affected by the size and series of the orders.

To attend to the above problems, Continuous Procedure introduced a V2 “Curie”. The significant enhancements consist of:

- It developed Uniswap V3 into the initial vAMM swimming pool and produced a liquidity swimming pool in the kind of v-token (such as vETH/vUSDC). When traders deposit USDC to open a position, the take advantage of liquidity service provider will create and input the quantity equivalent to that of the position. This is likewise a method of minting artificial possessions. The only distinction is that it utilizes a liquidity swimming pool included real tokens to change the initial mathematic solutions.

- Presenting the function of makers to offer liquidity management for Uni V3 can enhance its liquidity to some degree. However the liquidity of the swimming pool depends upon the funds and market-making capability of the makers.

- The Insurance Coverage Fund might be utilized to cover irregular settlements and function as the counter-party when there is an imbalance in between long and brief positions to offer more liquidity to the swimming pool.

It appears that the AMM option utilized by Continuous V1 can offer unrestricted liquidity, however it will experience unavoidable effect expense when a bigger quantity of funds is included. The updated V2 design is likewise based on the capability of makers. Liquidity service providers who utilize the active market-making method of Uni V3 might likewise bear the impermanent losses. Although the AMM design has actually dealt with the long tail issue of the derivatives market, its effect expense is still high for massive and price-sensitive traders.

Order book design represented by dYdX

The locked quantity and earnings stats of dYdX. Source: Token terminal

As one of the earliest trading platforms for decentralized derivatives, dYdX introduced its very first BTC-USDC continuous futures last May. It went on to co-built a Layer 2 option for cross margin perpetuals on the StarkEX engine together with StarkWare this April. Apart from supporting perpetuals, dYdX likewise uses loaning, area trading and margin trading. Its futures trading volume ranks 2nd in the decentralized perpetuals market, representing 12%.

Embracing the order book design with Wintermute as its leading maker to offer liquidity, dYdX combines off-chain matching with on-chain settlements. For that reason, the deal design is generally the like CEX, with the deal rate identified by the market value, which remains in turn set by the maker. According to information launched by Wintermute, 95% of the existing deals on dYdX are estimated by makers, making them the core strength for order-book-based platforms. This is the reason most critics slam dYdX for being too centralized.

The order book design is extremely requiring on the efficiency of matching and deals. It generally runs like this: StarkEX will get a series from dYdX, runs them internally, and guarantees that whatever is had a look at and significant. Then, it moves the deal to the Cairo program. The Cairo compiler will put together the Cairo program, and after that the prover will transform it into a STARK evidence. Then, the evidence will be sent out on this chain to the verifier for confirmation. The evidence is legal if it is accepted by the verifier. So everybody can examine the account balance of all users on Layer 1 however the deal information is not produced on the chain. In this method, it safeguards the personal privacy of the deal method and decreases deal expenses. At the exact same time, the gas cost on Layer2 will be borne by the dYdX group. Users just require to pay a deal cost.

As Layer2 and other scaling options enhance in time, the user experience of order-book deals will quite look like that of a DEX. In addition, advanced orders have actually been introduced by dYdX, consisting of market orders, limitation orders, Take earnings and Stop loss, Good-Till-Date, Fill Or Eliminate or Post-Only, providing traders futures trading services that are significantly comparable to those of central exchanges. For a future exchange, there are various top priorities at numerous phases. For instance, relying entirely on makers is a required method to keep liquidity in the early days. As expert financiers going into the marketplace, the whole environment will develop and end up being less centralized.

Artificial possessions design represented by Synthetix

The locked quantity and earnings stats of Synthetix. Source: Token terminal

As the earliest and biggest artificial possessions platform, the advancement of Synthetix is popular to the majority of the readers and will not be elaborated here. On Synthetix, users stake SNX to create sUSD based upon a collateralization ratio of 500%, and after that exchange the sUSD into any artificial possessions within the system through deal. They can go long on sToken, or go brief on iToken. The possessions to be negotiated are not restricted to cryptocurrencies, however consist of Forex, stock and products. In our conversation, artificial possession is noted as one of the deal designs for decentralized derivatives since it is likewise a type of futures agreement traded with security, or margin.

The deal design of SNX is relatively brand-new because it presents the principle of a “vibrant financial obligation swimming pool”. The financial obligation borne by the users and the system will alter in real-time. When a user stake SNX to mint sUSD, the sUSD ends up being the financial obligation of the system. When the users transform the sUSD into sToken, the financial obligation of the system will develop as the worth of the sToken modifications. And such financial obligation is shared proportionately by all users who have actually staked SNX. Let’s take a look at an example:

Expect there are just A and B in the system. They each minted 100 sUSD.

| A’s financial obligation | B’s financial obligation | Overall financial obligation | |

| Mint 100 sUSD | 100 sUSD | 100 sUSD | 200 sUSD |

| An utilizes them to purchase sBTC; B holds them | 100 sUSD | 100 sUSD | 200 sUSD |

| BTC rate doubles( prior to financial obligation circulation) | 200 sUSD | 100 sUSD | 300 sUSD |

| BTC rate doubles( after financial obligation circulation) | 150 sUSD | 150 sUSD | 300 sUSD |

Ultimately, their financial obligations are both 150 sUSD, however A’s possession worth reached 200 sUSD while B’s possession stayed 100 sUSD. At this moment, if An offers sBTC to get 200 sUSD, then he will just require 150 sUSD to redeem SNX, while B will require to purchase 50 sUSD prior to redemption.

From this viewpoint, Synthetix’s financial obligation swimming pool design is really a vibrant zero-sum video game. The earnings might originate from the increase in the rate of one’s own possessions, or the fall in the rate of other individuals’s possessions; vice versa. Or we can state, stakers on Synthetix are really going long on “their own financial investment capability/the financial investment ability of other individuals” You might likewise hold sUSD in the long term, however this will put you at the danger of “I might lose cash since other financiers are too capable.” As Taleb states, by staking SNX to create sUSD, users have skin in the video game. The strong style of risk-sharing turn all users into genuine “stakeholders”.

Source: Mint Ventures https://www.chainnews.com/articles/894865830615 htm

This strong and imaginative style of SNX is basically comparable to the zero-sum video game integrated in the AMM design. And for vAMM, its procedure of inputting virtual possessions based on the quantity of employment opportunities likewise looks like the minting of artificial possessions. The distinction is that Synthetix, fed by an oracle maker, does not need to fret about rate slippage or the circulation of possessions. In this method, it offers the users with really unrestricted liquidity.

Present Issues for Decentralized Derivatives Exchanges

After highlighting on how decentralized derivatives items run, let’s return to the issues noted at the start of this short article. Can they be resolved by the above jobs? What’s the future of decentralized derivatives items?

Efficiency

The efficiency problems are now being partially attended to, with numerous decentralized derivatives platforms embracing various scaling alternatives: Continuous Procedure utilizes the sidechain option xDai; dYdX embraces Layer2 option based upon ZK-rollup innovation to perform off-chain matching and on-chain record-keeping; SNX carries out a Layer2 scaling option “Optimisitc”. These scaling options have actually attended to the need for real-time deal and the front-run issue throughout deal execution.

Cost Discovery

For the AMM design, costs are generally specified by possessions within the swimming pool and the formula of x * y= k. The execution rate is independent from an external oracle, however the financing cost utilizes Chainlink’s rate feed as the index rate. The Continuous V2 likewise will integrate Uniswap oracle after presenting the liquidity swimming pool of Uni V3. The AMM design is for that reason less prone to oracle failures.

On dYdX, 3 various costs are utilized: index rate, oracle rate and mid-market rate. Amongst them, the index rate is kept by the dYdX group. It is identified by referencing the costs of 6-7 area exchanges and is utilized to activate conditional orders. The oracle rate is offered by Chainlink and MakerDao for the estimation of margins and financing charges. The mid-market rate is the rate produced by the order book, likewise utilized to compute the financing charges. The rate discovery design of dYdX resembles CEX where the execution rate is based upon the order book while liquidation rate is identified by the oracle. On the whole, the rate of dYdX is generally affected by makers and arbitrageurs, however its liquidation rate might be impacted by the dangers of oracle breakdown.

In contrast, SNX utilizes Chainlink decentralized oracles to power all rate eat its platform, consisting of the deal rate, system financial obligation and liquidation rate.

Threat Control

We can see that practically all derivatives exchanges count on oracle costs for liquidation, which happens when the position margin ratio is up to a specific level. In such cases, the users will be compensated through the system of Insurance coverage Fund. Considered that the majority of the jobs depend on the quotes of Chainlink, the danger of oracle attack appears to be inescapable. Furthermore, the on-chain liquidation blockage issue triggered by violent rate swings stays unsolved, yet it might be reduced through scaling options in the future.

Expense and Liquidity

The issue is twofold: little volume traders require to bear greater gas charges, and big volume traders need to pay greater effect expenses triggered by liquidity. While the previous has actually been partially dealt with through Layer2 options, the latter is more complicated. It can be rather challenging to evade in the AMM design; for platforms based upon order books, it might depend upon the market-making capability and capital size of the makers; for artificial possessions, the effect expense of a single trader might be smoothed out if the capital size of the total procedure is big enough.

In addition, deal charges can be another issue for derivatives traders with a greater turnover rate. From the existing stats, the deal charges of DEXes are much greater than those of CEXes. For instance, Continuous Procedure charges 0.1% for each deal, while dYdX gathers a maker cost of 0.05% and a taker cost of 0.2% for regular users, compared to 0.02% -0.04% in central exchanges. Despite the fact that all the above jobs have actually introduced the trans-fee mining function to compensate the deal charges, the last deal expense in DEXes is still reasonably high.

Capital Usage

In regards to capital usage, the DEXes based upon AMM and order books are not extremely various from CEXes. The upkeep margin ratio is 6.25% for Continuous Procedure and 7.5% for dYdX. However derivatives exchanges based upon artificial possessions, such as SNX, need a 200% overcollaterization to prevent liquidation. Though SNX can offer unrestricted liquidity, the overcollaterization system puts considerable constraints on capital usage, which breaks the intent of futures trading.

Privacy

The existing scaling options of all exchanges are moving the majority of the deal information to off-chain. Take dYdX for instance, it utilizes “zero-knowledge evidence” to secure the personal privacy of users. It can be anticipated that the privacy of futures will be ensured as privacy-focused layer2 options enhance in time.

Conclusion

From the above contrast in between decentralized derivatives exchanges, we can see that the order-book platforms represented by dYdX can much better fix the significant discomfort points of currents derivatives items. Their deal designs and functions are likewise more in line with the practices and requirements of derivatives traders. Critics might implicate dYdX of not being decentralized enough, however really, it is simply a tactical option in between survival and advancement at various phases. After all, the main objective of a decentralized job is to satisfy the standard requirements of users, while decentralization might be slowly accomplished by engaging more organizations and varied individuals to boost the environment.

Like fresh fruit and vegetables in e-commerce confronted with numerous restrictions in items, innovation, and channels, derivatives likewise discover it challenging to break barriers. It is for that reason not most likely for decentralized derivatives exchanges to shock the dominant position of CEXes. Nevertheless, with the advancement of Layer2 and other scaling options, their issues concerning efficiency, danger control, deal expense and privacy will be partly resolved. It is reasonable to state decentralized derivatives exchanges will end up being the greatest recipient of Layer2 innovation. From a long-lasting point of view, derivatives trading is still among the most appealing sectors with unrestricted possibilities.

NewsBTC Read More.

Value Prediction: Can This Recent Inverse Head-and-Shoulders Sample Open a Path to $595?")