It has actually been more than a year considering that the NFT boom in2021 According to NFTGO, the marketplace cap of NFTs peaked at $368 billion in March2022 As the marketplace later on cooled, the trading volume and market cap of NFTs began to diminish. This crypto novelty broadened its impact beyond the crypto neighborhood and promoted a big market, which likewise triggered the mix of NFTs and DeFi. The marketplace has actually experienced the look of NFT financing platforms, NFT aggregators, and NFT derivatives markets, which makes up the 2nd launching of DeFi Lego allowed by NFTs. Nevertheless, one questions whether these items were developed to satisfy genuine market needs and if they have actually produced an incorrect proposal that does not have any worth for market involvement. Today, we will dive into whether NFT-fi is a possible pattern and if it will make market acknowledgment.

It has actually been more than a year considering that the NFT boom in2021 According to NFTGO, the marketplace cap of NFTs peaked at $368 billion in March2022 As the marketplace later on cooled, the trading volume and market cap of NFTs began to diminish. This crypto novelty broadened its impact beyond the crypto neighborhood and promoted a big market, which likewise triggered the mix of NFTs and DeFi. The marketplace has actually experienced the look of NFT financing platforms, NFT aggregators, and NFT derivatives markets, which makes up the 2nd launching of DeFi Lego allowed by NFTs. Nevertheless, one questions whether these items were developed to satisfy genuine market needs and if they have actually produced an incorrect proposal that does not have any worth for market involvement. Today, we will dive into whether NFT-fi is a possible pattern and if it will make market acknowledgment.

Figure 1: Market Cap & Volume of NFTs|Source: nftgo.com|Since June 1, 2022

There are numerous NFT liquidity options and NFT structured items in today’s market:

1. NFT fragmentation: feet tokens (such as ERC20 tokens) that are provided by dividing the ownership of important NFTs. NFT fragmentation jobs consist of Fractional.art, NFTX, and so on

2. NFT financing markets: Holders can obtain short-term loans by collateralizing their NFTs without offering them. Popular NFT financing markets consist of BendDAO, NFTfi, and Drops DAO.

3. NFT leasing: Holders make leas by renting NFTs to users in requirement. NFT leasing jobs consist of Double, reNFT, and so on

4. NFT aggregators: These aggregators, such as Gem.xyz, combine the deal information of several NFT exchanges, acquire the very best NFT deal rate in one stop, and offer users with increased liquidity and more alternatives.

5. NFT derivatives: NFT derivatives consist of NFT alternatives like Putty, in addition to NFT continuous futures agreements such as NFTprep.

These jobs are early efforts to combine NFTs and DeFi. In specific, NFT fragmentation jobs and NFT aggregators resolve the issues of bad NFT liquidity and high market limit. NFT financing markets and NFT leasing jobs likewise concentrate on enhancing NFT liquidity and capital usage. On the other hand, NFT derivatives are more intricate structured items developed to enhance capital usage. Nevertheless, these jobs have actually not had the ability to accomplish massive adoption due to the fact that they deal with restrictions in regards to the underlying NFT reasoning and the advancement area. Next, we will check out the genuine needs and incorrect proposals of NFTs.

Genuine Needs

1. The capital usage of NFTs requires to be enhanced, permitting holders to collateralize their NFTs for partial liquidity when lacking money.

2. The liquidity issue of NFTs ought to be attended to, making it possible for holders to rapidly buy/sell the NFTs they own.

Incorrect Proposals

Did the capital usage of NFTs go higher?

The issue of NFTs’ capital usage can be seen in 2 elements: 1) Users require to rapidly purchase and offer NFTs, and the deal frequency ought to not be impacted by the bad liquidity of NFTs; 2) Users ought to have the ability to rapidly exchange their NFTs for liquidity and acquire money for other functions. When it pertains to feet tokens, capital usage can be enhanced through staking, utilize, and so on. Nevertheless, in the NFT market, there are just a couple of methods through which users can enhance their capital usage. In addition, integrating financing with NFT substantially increases the discovering expense. Today, most NFT holders still count on the “purchase low and offer high” method. Additionally, most such holders are not the target user of NFT financing jobs due to the fact that just blue-chip NFTs with sound liquidity and worth agreement are accepted.

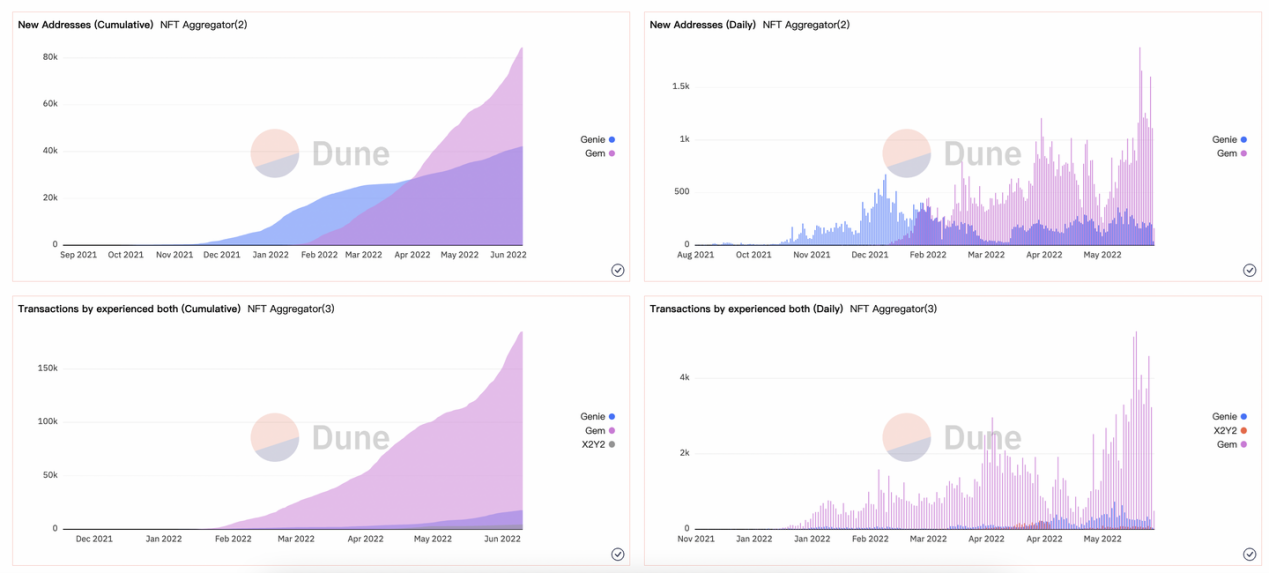

In regards to the total market scale, a lot of users are taken in by secondary markets and aggregators with low operating limits, and they have actually not accomplished any significant enhancement in capital usage. As displayed in Figure 2, the variety of brand-new addresses of Genie and Gem, 2 NFT aggregators, has actually been on a stable increase, with significantly regular everyday deals. Nevertheless, as the trading volume and deal frequency of the 2 have actually been struck by the slow market conditions of NFTs, Genie and Gem have yet to reach their optimal capacity for enhancing the capital usage of NFTs.

Figure 2: New Addresses and Deals of NFT Aggregators|Source: Dune @sohwak

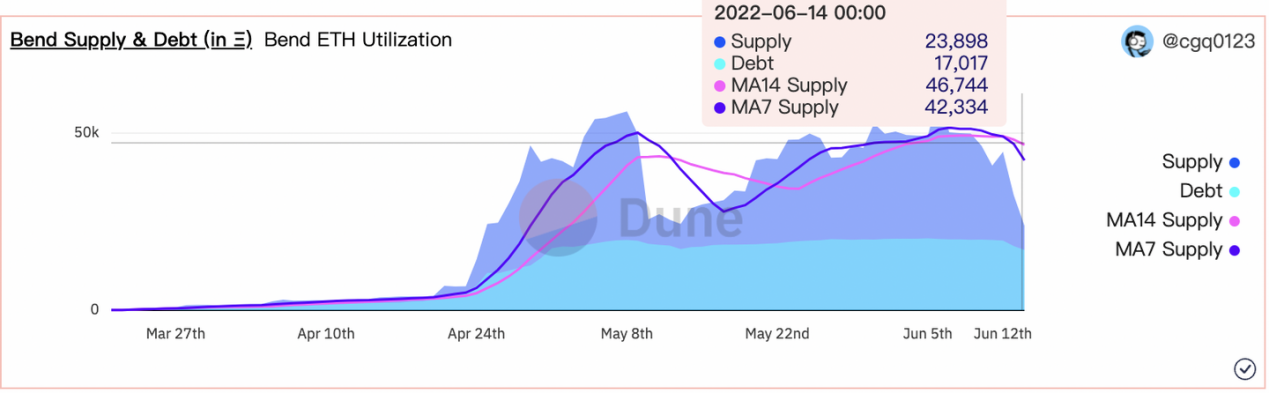

Let’s rely on the capital usage of traditional financing jobs. BendDAO is a loaning market based upon the liquidity swimming pool design where holders can obtain ETH from the swimming pool after collateralizing their blue-chip NFTs. Due to current market changes, a big quantity of ETH deposit in BendDAO’s liquidity swimming pool has actually been withdrawn, which led to reduced ETH supply. Yet, the ETH loans have actually stayed at around 19,000 ETH, while the MA14 supply stands at 46,000 As such, we can make the rough quote that BendDAO’s capital usage has to do with 41%.

Figure 3: Bend ETH Usage|Source: [email protected]

Note: MA14 describes the moving average in 14 days, while MA7 shows the moving average in 7 days

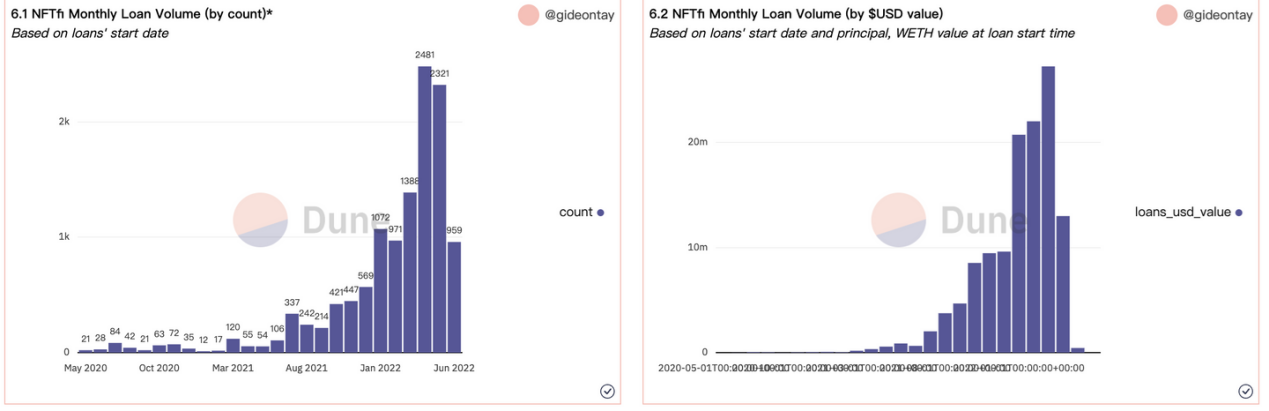

NFTfi is a loaning market following the P2P design. The quantity, rate of interest, and period of loans on NFTfi are collectively identified by liquidity service providers and NFT loan providers, which is more versatile in regards to the loan rate. The variety of month-to-month loans used by means of NFTfi increased from 21 in May 2020 to 2,000+ in May 2022, and the optimum month-to-month loan quantity reached $2752 million (March 2022), however this figure just represented 1% of the marketplace cap of blue-chip NFTs (as reported by NSN-BlueCHIP 10).

Figure 4: NFTfi Regular Monthly Loan Volume by Count/Value| Source: [email protected]

JPEG ‘d is likewise a P2P design financing procedure, and it now just offers collateralized financing for Cryptopunks, EtherRocks, BAYC, and MAYC. After staking NFT, holders will get PUSD, a stablecoin, supplied by the procedure from the swimming pool. Furthermore, JPEG ‘d likewise includes a 32% capital usage limitation on financing.

Obviously, there are likewise other early-stage NFT derivatives platforms, however they have actually not presented any fully grown items, so we might not examine their capital usage. In Spite Of that, it is foreseeable that such NFT derivatives will include greater knowing expenses as they are items developed for expert traders with higher threat hunger. As such, their development capacity is restricted in today’s NFT market.

Property Rates and Liquidation Dangers ?

The rates of NFTs has actually been so often gone over that it has now end up being a cliché. Individuals are interested in the problem due to the fact that the rate swings of NFTs will expose NFT financing or derivatives to liquidation dangers. As the NFT rates tipped over the current duration, BendDAO has actually begun numerous liquidation auctions.

Although the majority of the financing procedures out there have actually embraced over-collateralization, in the face of wild rate swings, numerous NFTs would be liquidated and offered in markets. This, paired with the bad liquidity of NFTs, may cause worry offering, which would produce down rate spirals, eventually turning the loans into uncollectable bills.

The rates of NFTs undergoes several aspects. Plus, it is likewise quickly controlled. For instance, huge holders might maliciously raise the flooring rate and after that liquidate the NFTs on function, and an NFT might take a cost plunge due to hacking or wise agreement loopholes. Additionally, NFT rates might likewise be impacted by numerous intangible aspects. For example, the rate of an NFT might skyrocket if a celebrity all of a sudden purchases it in big quantities or if it launches a brand-new airdrop strategy.

As a lot of loan providers can not properly approximate the intrinsic worth of their NFTs, they are susceptible to liquidation if they obtained loans or used utilize. This is likewise among the reasons NFT financing and derivatives have actually not acquired mass adoption: Blue-chip NFT holders are stressed that they may suffer losses in the above situations, which is why they hesitate to collateralize their NFTs.

Do blue-chip NFT holders truly require NFT loans?

All NFT financing markets concentrate on blue-chip NFTs, however a lot of blue-chip NFT holders are not in excellent requirement of loans. To start with, such holders care more about their ownership of the NFTs, much like billionaires would not utilize their antiques as security for loans. Second of all, NFT loans featured unidentified dangers, and numerous blue-chip NFT holders decline to look for such loans after weighing the dangers versus the advantages. Finally, obtaining NFT loans includes high knowing expenses, and not every user can comprehend the concept behind such loans.

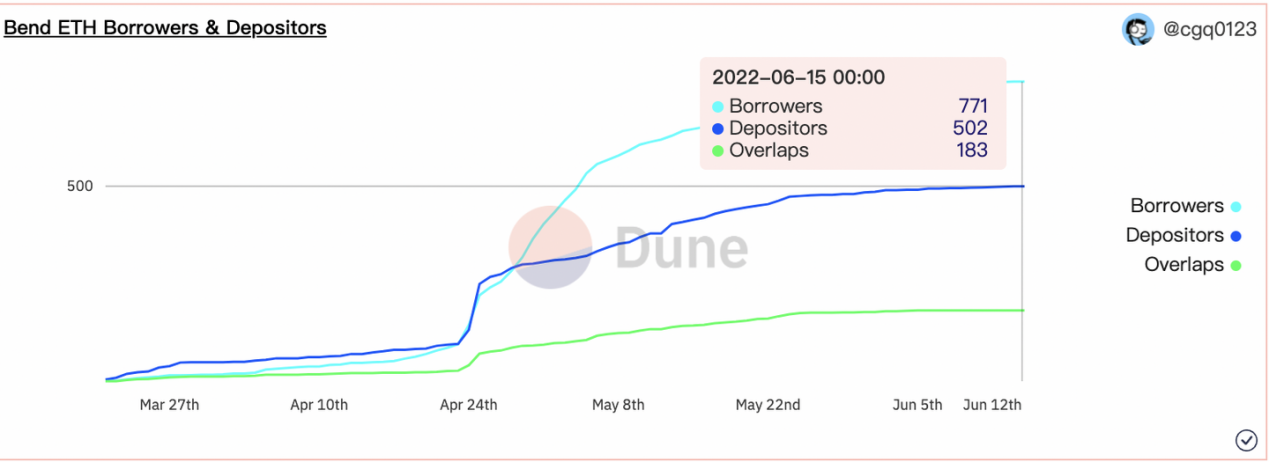

Let’s compare the user base of the significant NFT financing jobs. Since June 15, there have to do with 2.4 million holders in the NFT market, of which 27,833 hold blue-chip NFTs (a user will be considered as a blue-chip NFT holder as long as he owns a minimum of one such NFT), according to NFTGO. There are 771 debtors on BendDAO, 1,038 on NFTfi, and 51 on Game. As users should initially deposit/collateralize their NFTs prior to obtaining a loan, we can relate to all these debtors as blue-chip NFT holders. It is for that reason clear that a lot of blue-chip NFT holders are not users of NFT financing markets.

Figure 5: Bend ETH Customers & Depositors|Source: [email protected]

Could NFT-fi jobs keep users with the usual reward?

Financing or derivatives jobs likewise bear the job of enhancing the procedure’s liquidity. The majority of such jobs provide native tokens as the reward for hiring NFT holders and depositors as they go live. In this regard, these jobs look like DeFi liquidity mining platforms that draw in speculators with high APYs. Nevertheless, the issue is that they would not have the ability to keep such liquidity if the APYs decreased. Drawing in users with token rewards is still the usual method. Though this method might produce a big user base at the very start, nobody understands whether the procedure might keep users.

For instance, when the job was very first released, BendDAO airdropped BEND tokens to users who had actually transferred blue-chip NFTs and ETH. It likewise utilizes BEND as an aid when paying interests. Nevertheless, the rate of interest decreased when the BEND rate dropped, which decreased the development rate of brand-new users.

As such, drawing in users with high APYs is just the primary step. To keep brand-new users, they should even more check out the financing systems, resolve the oracle rates problem, and reduce the liquidation dangers. Tasks ought to establish more versatile items while broadening the scope of NFT financing. Lastly, they might likewise offer threat evaluations, lower the discovering expense, and provide more rewarding user experiences.

Conclusion

The advancement from NFT to NFT-fi is a procedure in which a market grows from its infancy to a more fully grown phase. Nevertheless, it is likewise undoubtedly a procedure that has plenty of doubts, traps, and issues. As NFT-fi jobs look for to satisfy genuine needs, they will likewise need to deal with doubts that they are mentioning incorrect proposals. Today’s NFT market resembles a newborn kid who requires to mature and stick through difficulties. Although NFT-fi may be a fantastic effort, there is still a long method to go, and NFT-fi jobs need to keep exploring their hidden reasoning to make market acknowledgment.

NewsBTC Read More.