Crypto markets are confronting a fast-moving repricing of US financial coverage expectations, and macro dealer Alex Krüger argues that even after final week’s sharp dovish flip, futures curves nonetheless fail to low cost what a Trump-aligned Federal Reserve management might appear like.

Fed Lower Mispricing Units Up Crypto Repricing Occasion

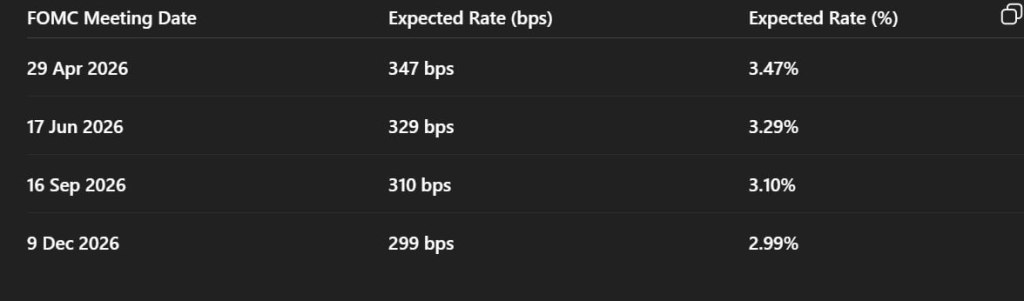

In a put up on X, Krüger shared a CME-derived desk of implied coverage charges for late-stage 2026 and framed it because the market’s baseline for the post-Powell transition. The desk reveals an anticipated fed funds price of three.47% for the April 29, 2026 FOMC assembly (347 bps), drifting to three.29% for June 17, 2026 (329 bps), to three.10% for September 16, 2026 (310 bps), and to 2.99% for December 9, 2026 (299 bps).

In different phrases, the curve costs roughly 48 foundation factors of easing between late April and early December 2026 about two quarter-point cuts throughout that span—implying a comparatively gradual descent towards slightly below 3%.

Krüger’s core declare is that this path is inconsistent with the coverage preferences he associates with the Trump camp, and subsequently inconsistent with an “extremely dovish” chair appointment. He situates the April 2026 assembly because the final one below Jerome Powell’s chairmanship, whose four-year time period ends in mid-Might 2026, after which treats the June 2026 assembly as the primary under a new chair.

Associated Studying

In opposition to that transition, Krüger factors to Fed Governor Stephen Miran—whom he casts as a proxy for Trump-world financial instincts—as advocating a a lot quicker return to impartial. In Krüger’s telling, Miran has argued that the “acceptable fed funds price” is “roughly 2% to 2.5%,” has linked this yr’s tighter stance to an increase within the impartial price, and has characterised his divergence from colleagues as centered on “pace of cuts,” not vacation spot.

Krüger additionally highlights Miran’s choice for “50 bps cuts” over 25-bp steps as the best way to get coverage again to impartial. On Krüger’s arithmetic, a futures curve that delivers solely about 50 bps of easing from the first post-Powell meeting in June 2026 by means of December 2026 will not be a curve that has really priced a Trump-era chair keen to front-load bigger strikes.

Associated Studying

Put merely, he sees the market as nonetheless anchored to a Powell-style glide path, even whereas political threat is skewing towards extra abrupt easing. “The Trump camp desires quicker and greater cuts, a lot of them. The Fed solely chopping 50bps between the brand new Fed Chair’s FOMC in June and December 2026 falls quick. That’s why I maintain an extremely dovish Fed Chair appointed by Trump will not be priced in,” Krüger concludes.

December Charge Lower Appears Possible

The timing of Krüger’s warning issues as a result of the entrance finish has already undergone a dramatic swing. Final week, merchants sharply elevated the likelihood of one other lower on the Fed’s December assembly after New York Fed President John Williams mentioned charges might fall “within the close to time period,” a comment that pushed implied odds of a quarter-point December transfer into the mid-70% vary on CME FedWatch, up from roughly 40% the day earlier than.

In parallel, Goldman Sachs chief economist Jan Hatzius reiterated a baseline through which the Fed cuts in December, then once more in March and June 2026, taking the coverage band right down to roughly 3.00%–3.25%.” We anticipate one other Fed lower in December, adopted by two extra strikes in March and June 2026 that take the funds price to 3-3.25%,” mentioned Hatzius.

GOLDMAN SEES DOWNSIDE RISKS FOR ECONOMY NEXT YEAR

Goldman Sachs economists anticipate the Fed to chop charges in December, adopted by a number of extra cuts in 2025, bringing charges simply above 3%. Chief economist Jan Hatzius warns the economic system might gradual greater than anticipated, requiring…

— *Walter Bloomberg (@DeItaone) November 24, 2025

His path is modestly extra dovish than what the curve had discounted earlier within the month, nevertheless it nonetheless resembles the gradualism embedded in Krüger’s CME desk: sequential 25-bp steps, aiming for an early-2026 price across the low-3% space moderately than a fast drop towards the low-2s.

For the crypto markets, the dispute is much less about whether or not cuts are coming than in regards to the pace and terminal price. Crypto is structurally levered to shifts in greenback liquidity and real-rate expectations; what Krüger is flagging is a situation the place the curve’s “vacation spot” and, particularly, its pacing stay too conservative relative to a possible political reorientation of the Fed.

If merchants are proper that the Williams-sparked repricing is the start of a slower, data-dependent easing cycle, then present crypto asset valuations already incorporate the related macro impulse.

If Krüger is correct, the curve continues to be lacking a regime change in response operate—one through which bigger front-loaded cuts compress money yields quicker than anticipated, steepen risk-on positioning, and pressure one other spherical of cross-asset period and liquidity repricing. That hole between a Powell-era slope and a Trump-era shock path is what he means when he says an ultra-dovish chair “will not be priced in” for crypto markets.

At press time, the overall crypto market cap was at $2.92 trillion.

Featured picture created with DALL.E, chart from TradingView.com

Jake Simmons Read More

Worth Prediction: Is the Weekly MA200 Setting the Stage for a $67Okay Breakout?")

Worth Prediction: Is the Weekly MA200 Setting the Stage for a $67Okay Breakout?")