The European Central Bank chosen ten know-how firms on October 2, 2025, to construct the infrastructure for its deliberate digital euro.

5 Essential Parts

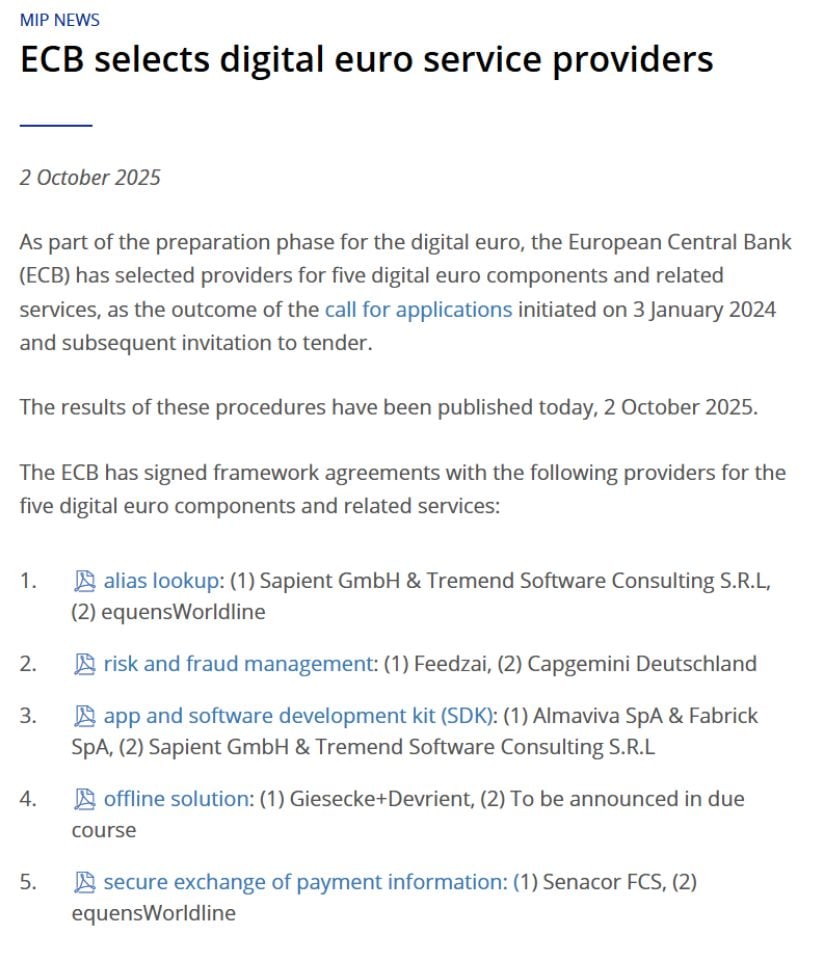

The ECB signed agreements with firms to deal with 5 key components of the digital euro system. The central financial institution began this course of in January 2024, reviewing functions from over 50 firms earlier than making ultimate choices.

Portuguese startup Feedzai won the contract for fraud detection and prevention, working alongside consulting agency PwC. The fraud administration part carries an estimated worth between €79.1 million and €237.three million. Feedzai’s AI-powered platform will analyze each digital euro transaction throughout the eurozone, offering fraud threat scores to assist banks determine whether or not to approve funds.

German safety firm Giesecke+Devrient, partnering with Nexi and Capgemini, secured the contract for offline funds. This function permits customers to make funds with out web connection whereas sustaining cash-like privateness. Cash shops instantly on units like smartphones or playing cards, with no data stored by banks, fee firms, or the ECB.

Sapient GmbH and Tremend Software program Consulting will deal with alias lookup providers, making it doable to ship cash utilizing cellphone numbers or e-mail addresses as a substitute of advanced account numbers. Italian firms Almaviva and Fabrick will develop the digital pockets apps and software program instruments. German agency Senacor FCS will handle safe info trade between monetary establishments.

Every part has a first-ranked and second-ranked supplier. The ECB will work with top-ranked firms initially, turning to backup suppliers provided that essential.

Privateness and Safety Take Heart Stage

The associate choices reveal what issues most to the ECB. Privateness safety and fraud prevention dominate the alternatives.

Supply: @ECB

The offline fee answer addresses the largest concern many Europeans have about digital currencies. Dr. Ralf Wintergerst, CEO of Giesecke+Devrient, defined the importance: “This milestone underscores our dedication to innovation and safety in digital fee options whereas preserving the privateness and resilience that residents count on from money.”

Funds settle regionally between units with no third-party involvement. No financial institution, fee supplier, or central authority can observe these transactions. The system works even with out energy or web connection.

For on-line funds, the ECB plans sturdy privateness protections together with pseudonymization and encryption. The central financial institution has said it won’t be able to determine customers or observe their purchases from the fee information it receives.

Feedzai’s fraud detection system should stability safety with privateness. CEO Nuno Sebastião described the problem: “With tens of billions of transactions anticipated throughout the eurozone, success depends upon AI that may adapt as shortly as fraud evolves.”

Timeline Stretches to 2029

The digital euro’s preparation section runs by way of October 2025. At that time, the ECB Governing Council will determine whether or not to maneuver ahead with the subsequent growth section.

Nonetheless, the precise launch depends upon European Parliament approval of the Digital Euro Regulation. ECB Government Board member Piero Cipollone lately said that mid-2029 represents a practical launch goal.

The framework agreements signed this week don’t contain speedy funds. They set up phrases for future work. Precise growth of the parts will solely start after the Governing Council decides to proceed and EU laws passes.

These agreements embody flexibility to regulate primarily based on modifications to the laws. This protects each the ECB and know-how companions as lawmakers debate and modify the regulatory framework.

Political Hurdles Stay Excessive

The digital euro faces critical political challenges. European Parliament approval stays the largest impediment.

Lawmakers have raised considerations about privateness, the affect on business banks, and whether or not the ECB can reliably function such a large client system. A March 2025 outage within the ECB’s Goal 2 fee system, which handles massive interbank transactions, intensified these doubts. The system didn’t settle transactions for a full day.

Euro-area finance ministers lately agreed on buyer holding limits for the digital forex, offering some progress. However parliamentary motion has been gradual for the reason that European Fee first proposed laws in June 2023.

The legislative schedule forward consists of tight deadlines. After a progress report anticipated in late October, lawmakers may have six weeks to suggest amendments and 5 months for negotiations.

Europe’s Response to Greenback Dominance

The digital euro goals to scale back Europe’s dependence on non-European fee techniques. At the moment, most digital funds circulate by way of American firms like Visa, Mastercard, and PayPal.

US assist for dollar-backed stablecoins has elevated urgency on the ECB. President Trump signed the GENIUS Act on July 18, 2025, establishing a federal regulatory framework for stablecoins.

Cipollone famous that the unfold of US stablecoins threatens to divert deposits away from European banks. The digital euro represents Europe’s effort to take care of management over its personal fee infrastructure.

In the meantime, non-public alternate options are transferring quicker. Nine major European banks introduced plans in September 2025 to launch their very own regulated euro stablecoin by mid-2026. Germany launched EURAU, its first regulated euro stablecoin, in July 2025.

The digital euro would work alongside money and financial institution deposits, not change them. The ECB designed it as a public good that advantages society relatively than a profit-making enterprise.

The Backside Line

The ECB’s number of know-how companions marks actual progress after 5 years of digital euro discussions. However the path from signed agreements to precise launch stretches years into the longer term.

Success requires coordination among the many ECB, nationwide central banks, European establishments, business banks, know-how suppliers, and lots of of thousands and thousands of residents. Political approval stays unsure. Public acceptance shouldn’t be assured.

The digital euro could reshape European funds by the tip of the last decade. Or it could grow to be one other delayed authorities undertaking overtaken by quicker non-public alternate options. The know-how basis is now being constructed. Whether or not something stands on that basis depends upon choices but to be made in parliamentary chambers throughout Europe.

Sven Luiv Sven Luiv Read More

Worth Prediction: BTC Nears Main Provide Zone as Bulls Goal a Break Above $65Ok")