Japan’s Monetary Providers Company (FSA) is contemplating a landmark reform that would let banks purchase and maintain cryptocurrencies like Bitcoin – a transfer that may lastly deliver conventional finance and crypto underneath one roof.

KEY POINTS:

➡️ Japan’s FSA is contemplating reforms that may let banks commerce and maintain Bitcoin, signaling a significant step towards institutional crypto adoption.

➡️ Over 12M crypto accounts in Japan spotlight sturdy retail demand as regulators transfer to make the market safer and extra clear.

➡️ Institutional entry may gasoline development for one of the best altcoins, particularly tasks with real-world utility and scalable infrastructure.

➡️ Bitcoin Hyper, Greatest Pockets Token, and Remittix stand out as early movers prepared to learn from Japan’s upcoming crypto wave.

With over 12M crypto accounts already open in Japan (3.5x greater than 5 years in the past), the nation’s urge for food for digital belongings is simple.

The FSA’s plan contains letting banks register as licensed crypto change operators and creating a brand new ‘Crypto Bureau’ to supervise the sector.

A separate 2026 invoice can also be within the works to crack down on insider buying and selling and enhance market transparency. Collectively, these steps sign Japan’s intent to make crypto safer and extra institution-friendly.

If banks and enormous traders achieve entry to crypto, they received’t simply purchase Bitcoin and Ethereum – they’ll search for scalable, utility-driven tasks with sturdy fundamentals.

That would put the highlight on one of the best altcoins and early crypto presales poised to develop as institutional cash flows in.

1. Bitcoin Hyper ($HYPER) – The Quickest Layer-2 Turning Bitcoin Right into a Full-Energy Blockchain

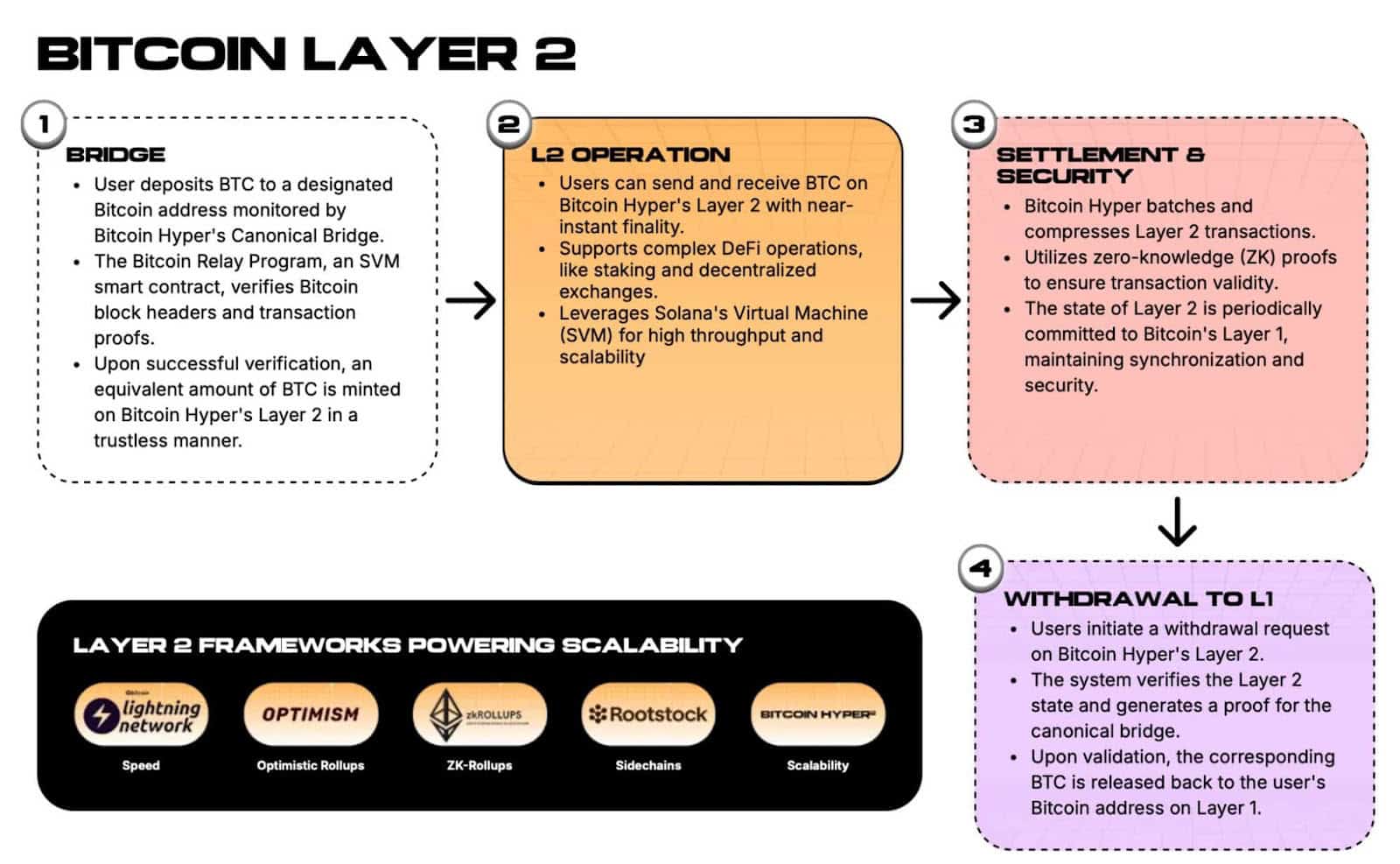

Bitcoin Hyper ($HYPER) is an actual Layer-2 constructed to rework the world’s greatest cryptocurrency from a ‘retailer of worth’ right into a residing, respiratory ecosystem.

Utilizing the Solana Digital Machine (SVM), Bitcoin Hyper delivers sub-second transactions and near-zero fuel charges, creating a spot the place funds, DeFi, dApps, and even meme cash can lastly thrive on Bitcoin.

Consider it as Bitcoin’s execution layer, the place velocity, interoperability, and tradition meet.

Builders can construct straight on high of Bitcoin Hyper, whereas customers get pleasure from seamless cross-chain motion between Bitcoin, Solana, Ethereum, and past. It’s a full-blown blockchain designed for builders, degens, and establishments alike.

With $HYPER priced at $0.013135 and over $24.1M raised in presale, this challenge is catching severe traction.

And if Japan’s banks begin getting into the crypto scene, infrastructure-grade tasks like HYPER may very well be the primary to really feel the institutional elevate.

Get in early on real Bitcoin innovation with Bitcoin Hyper.

2. Greatest Pockets Token ($BEST) – The Utility Token Fueling a Quick-Rising Crypto Ecosystem

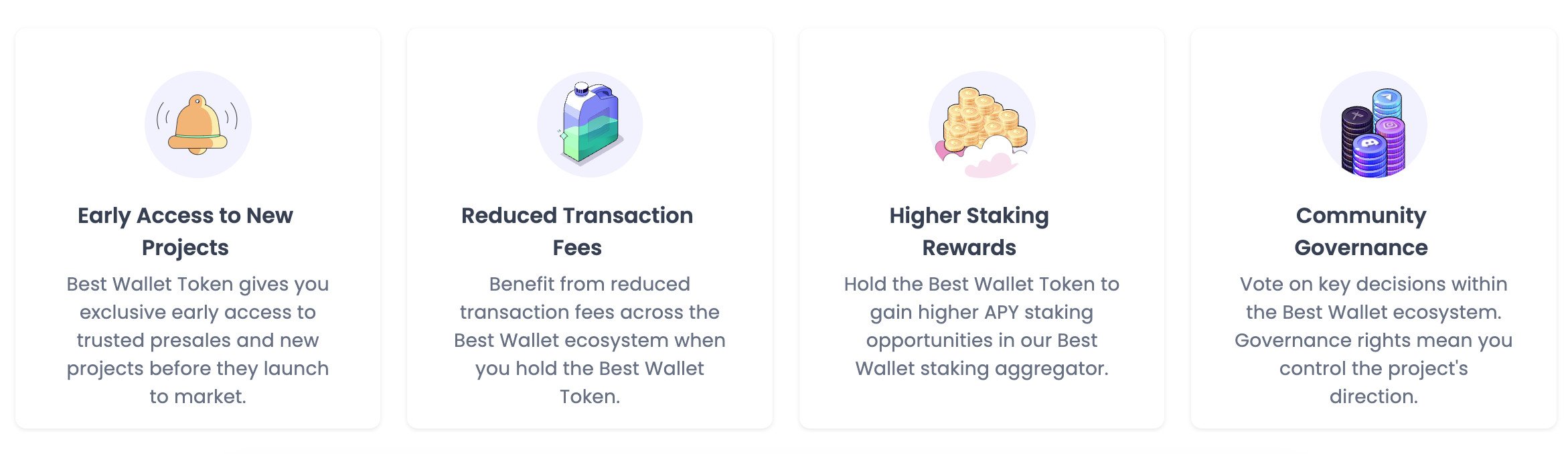

Best Wallet Token ($BEST) is the spine of a quickly increasing ecosystem constructed for the subsequent wave of crypto adoption.

Whereas its mum or dad platform, Best Wallet, delivers a modern multi-chain expertise, the $BEST token powers every little thing inside it – from lowered transaction charges and staking rewards to early entry to new crypto presales and unique challenge launches.

Holding $BEST means being a part of a rising economic system somewhat than a single app.

Token holders get pleasure from premium advantages and governance rights, positioning them on the middle of the platform’s development.

The challenge’s ‘Upcoming Tokens’ characteristic, which lets customers be a part of presales safely from inside the app, straight drives $BEST’s demand – each new challenge and transaction strengthens the token’s utility.

With $0.025815 per token and over $16.5M raised in presale, $BEST is attracting each retail and institutional curiosity.

If Japanese banks start getting into crypto markets, tokens tied to actual utility and adoption, like $BEST, may surge in relevance.

Grab $BEST now to secure your stake in the next big crypto economy.

3. Remittix ($RTX) – The PayFi Altcoin Bringing Banks and Crypto Collectively

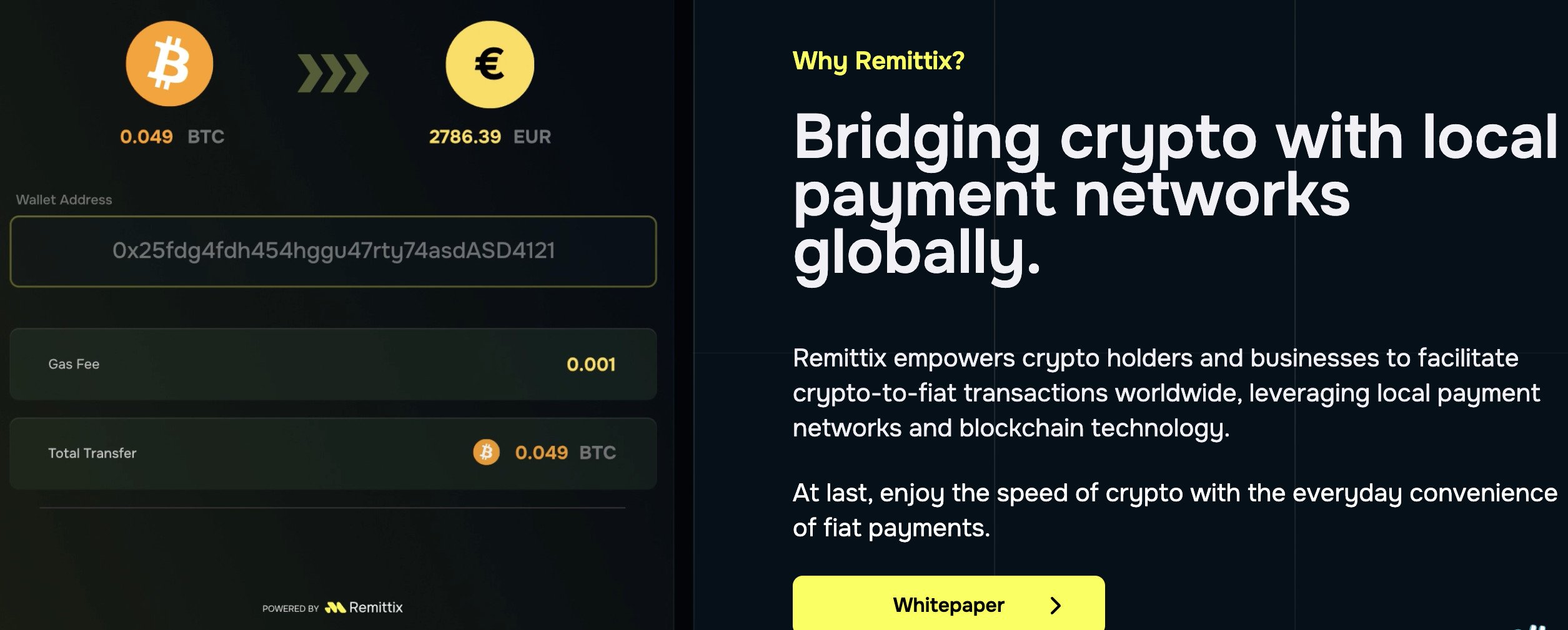

Remittix ($RTX) is redefining how cash strikes throughout borders.

Constructed as a PayFi protocol, it connects crypto wallets and conventional financial institution accounts in over 30 international locations, providing lightning-fast transfers, minimal charges, and actual exchange-rate transparency.

As a substitute of counting on sluggish, outdated SWIFT networks, Remittix makes use of blockchain rails to settle funds in seconds – all whereas preserving compliance and KYC frameworks bank-friendly.

Because the FSA considers letting banks commerce and maintain crypto, tasks like Remittix may bridge the hole between conventional finance and digital belongings, turning what’s now experimental into on a regular basis monetary infrastructure.

For banks exploring blockchain funds, $RTX provides a ready-made ecosystem that blends real-world utility with on-chain effectivity.

At $0.1166 per token and $27.5M raised in presale, Remittix has rapidly turn out to be among the best altcoins within the funds area of interest. It’s a possible spine for the subsequent era of cross-border finance.

Get into $RTX early and ride the wave as PayFi meets institutional crypto adoption.

Should you’re scanning the horizon for one of the best altcoins prepared to learn from the institutional wave, $HYPER, $BEST and $RTX provide distinct angles – infrastructure, utility pockets and finance-payments respectively.

This text is for informational functions solely and doesn’t represent monetary recommendation. At all times do your personal analysis (DYOR) earlier than investing in crypto.

Disclaimer: This content material has been provided by a 3rd celebration contributor. Courageous New Coin doesn’t endorse or promote any services or products talked about herein. Readers are inspired to conduct unbiased analysis earlier than making any monetary choices. The data supplied is for informational and academic functions solely and shouldn’t be interpreted as funding recommendation.

Benjamin Wallis Benjamin Wallis Read More

Presale Momentum Builds – Is It The Finest Crypto Presale?")

: Which is the Finest Crypto to Purchase 2026?")

Ranks Quantity One")